Buying property in Spain remains one of the most attractive investment opportunities for international buyers in 2025, but the legal and financial landscape has evolved significantly—especially for UK nationals navigating post-Brexit regulations. In 2023—the last full year for which we have statistics—more than 87,000 properties were purchased in Spain by foreign buyers. This represented 15% of the total number of conveyances that took place, up from 13.7% the previous year. These figures demonstrate that despite regulatory changes and economic headwinds, Spain continues to welcome a robust international property market.

Whether you're a British retiree seeking a Mediterranean haven, an American digital nomad exploring residency options, or a European investor diversifying your portfolio, understanding the step-by-step legal requirements, tax obligations, and regional market dynamics is non-negotiable. This comprehensive guide consolidates everything you need to know before signing a single document: from Brexit-related tax changes and visa pathways to financing challenges, notary costs, and the critical due diligence checks that protect you from fraud.

Spain's property market in 2026 is characterized by near-complete recovery to pre-financial-crisis price levels, tightening mortgage conditions for non-residents, and an increasingly complex regulatory environment for foreign buyers. The golden question is no longer whether you can buy property in Spain as a foreigner—you absolutely can—but rather how to navigate the process strategically, cost-effectively, and legally. This article is structured around the real questions international buyers ask lawyers in Spain every day, with a focus on transparency, pitfall prevention, and actionable legal guidance.

Want to hear what other clients

are saying about us?

1. The Impact of Brexit: Buying Property & Taxes for UK Nationals

Brexit fundamentally reshaped the legal status of British property buyers in Spain, transforming them overnight from EU citizens with freedom of movement into "third-country nationals" subject to the same visa, residency, and tax rules as Americans, Canadians, and other non-EU buyers. This section consolidates the scattered post-Brexit implications into a unified narrative, addressing the top concerns of UK nationals: whether they can still buy property, how long they can stay, and what tax penalties now apply.

Image: The post-Brexit legal landscape for UK property buyers in Spain, illustrating one of the biggest changes foreign buyers have faced in recent years.

Can British People Still Buy Holiday Homes in Spain?

Yes, British citizens can still buy property in Spain after Brexit. There are no legal restrictions preventing UK nationals from purchasing real estate—whether a holiday home on the Costa del Sol, a retirement villa in the Balearic Islands, or a buy-to-let investment in Barcelona. Despite Brexit, many British expats continue to buy property in Spain, and the Spanish government has implemented measures to facilitate property purchases for foreign buyers. The legal process remains identical: you will need a Spanish NIE number, a bank account, and independent legal representation, but your nationality does not disqualify you from ownership. In fact, British buyers remain one of the largest foreign buyer demographics in Spain, second only to Germans in many coastal regions.

What Are the Rules for Buying Property in Spain After Brexit?

The core change is that British nationals, now legally non-EU nationals, have different residency rights from prior to Brexit. If you plan to use your Spanish property purely as a holiday home and visit occasionally, the purchase process itself is unaffected. However, the 90/180-day rule now applies: UK citizens can stay in Spain (and the broader Schengen Area) for a maximum of 90 days within any 180-day period without a visa. Exceeding this limit without obtaining formal residency can result in fines, deportation, and bans on re-entry. If you intend to spend more than three months per year in Spain, you must obtain a residency visa before moving—simply owning property does not grant you the legal right to reside long-term. For detailed pathways, see moving to Spain from the UK.

Image: The relocation considerations facing UK buyers post-Brexit, from visa applications to tax residency planning.

Can I Buy a Property in Spain as a Non-Resident?

Absolutely. Non-residents—whether British, American, or any other nationality—can freely buy property in Spain, often using their properties as holiday homes and renting them out when not in use. The Spanish legal framework does not differentiate property ownership rights based on residency status. However, non-residency has significant financial implications: you will face stricter mortgage lending criteria (typically a maximum 70% loan-to-value ratio compared to 80% for residents), higher interest rate premiums, and different tax treatment on rental income and capital gains. You are also required to appoint a fiscal representative in Spain if you earn rental income as a non-resident, and you must file annual non-resident income tax returns. For comprehensive tax planning, consult resources on property tax in Spain.

Tax Implications of Brexit for UK Buyers

Brexit triggered a major change in the tax treatment of UK nationals, particularly regarding rental income. Under Article 24.6 TRIRNR (the relevant legislation regulating the taxes payable by any EU citizen who derives an income from rental properties in Spain), UK nationals are no longer eligible for the favorable 19% tax rate reserved for EU residents. Instead, British landlords now pay a 24% non-resident income tax rate on Spanish rental income—the same rate applied to US, Canadian, and other non-EU landlords. This 5-percentage-point increase can significantly erode net rental yields, especially in lower-margin buy-to-let markets.

Image: Tax changes for UK nationals post-Brexit, highlighting the shift from 19% to 24% non-resident income tax on rental earnings.

Similarly, when selling Spanish property, UK nationals are now subject to a 3% capital gains withholding tax at the point of sale (the same as all non-EU sellers), rather than the 19% rate that applied to EU nationals. The withheld amount is held by the Spanish Tax Agency as a deposit against your final capital gains liability, which is calculated at 19% for gains up to €6,000, 21% for gains between €6,000 and €50,000, and 23% for gains above €50,000. If the 3% withholding exceeds your actual liability, you can reclaim the difference—but this requires filing a tax return and often takes 12–18 months. For detailed guidance, see capital gains tax as non-EU residents.

Do Expats Pay Local Taxes?

Yes, all property owners in Spain—whether resident or non-resident, British or otherwise—are liable for local property taxes. The most significant is the IBI (Impuesto sobre Bienes Inmuebles), Spain's equivalent of council tax, levied annually by municipal authorities and typically ranging from 0.4% to 1.1% of the cadastral value of the property. This tax funds local services such as rubbish collection, street lighting, and infrastructure maintenance. If you are resident in Spain, you are also liable to the Spanish government to pay taxes on your worldwide income, including pensions, dividends, and rental income from other countries. Non-residents, by contrast, are only taxed on Spanish-source income (such as rental income from your Spanish property) and must pay a separate annual non resident income tax of 19% (for EU nationals) or 24% (for UK and other non-EU nationals) on the deemed rental value of the property, even if you do not actually rent it out. For a full breakdown, see Council Tax in Spain.

⚠️ Legal Warning: Many UK buyers mistakenly believe that purchasing property in Spain automatically grants them the right to live there year-round. This is false. Property ownership and residency rights are entirely separate legal issues post-Brexit, and overstaying your 90-day allowance can result in severe penalties, including bans on future Schengen entry.

2. Visas and Residency: Can You Live in Spain?

One of the most common misconceptions among international property buyers is the belief that purchasing real estate in Spain automatically grants you the legal right to reside there. It does not. Owning property and obtaining residency are two entirely separate legal processes, governed by different regulatory frameworks. This section clarifies the visa pathways available to non-EU buyers—including British, American, and other nationalities—and explains how to legally extend your stay beyond the 90-day tourist limit.

How Long Can I Live in Spain if I Buy Property?

Owning property in Spain does not determine your length of stay. Your permitted duration is governed exclusively by your nationality and visa status. Non-EU citizens (including British nationals post-Brexit, Americans, Canadians, and Australians) can stay in Spain for a maximum of 90 days within any 180-day period under the Schengen tourist visa waiver. This rule applies whether you own a €100,000 apartment or a €5 million beachfront estate. If you wish to spend more than three months per year in Spain—whether continuously or cumulatively across multiple trips—you must obtain formal residency authorization before moving. The 90/180-day clock is strictly monitored via passport stamps and electronic border systems, and exceeding it can trigger automatic fines (starting at €500), deportation, and multi-year bans on re-entry to all Schengen countries.

Can I Live in Spain Full Time if I Buy a Property?

You can live in Spain full-time, but only if you obtain a valid residency visa. EU citizens retain freedom of movement and can live year-round in Spain simply by registering as residents at their local town hall (a process called empadronamiento) and applying for a green residency certificate (certificado de registro). They do not need a visa. British nationals and other non-EU citizens, however, must apply for and be granted a specific residency visa before relocating. Fortunately, Spain offers several visa routes designed explicitly for property buyers, retirees, and remote workers. These include the Golden Visa (for high-value property investors), the Non-Lucrative Visa (for retirees and financially independent individuals), and the Digital Nomad Visa (for remote employees and freelancers). Each has distinct financial, legal, and documentation requirements.

How to Legally Stay in Spain for More Than 90 Days?

To exceed the 90-day tourist limit, you must obtain one of the following residency visas:

Golden Visa Spain: Designed for high-net-worth investors, this visa grants you and your immediate family members (spouse and children under 18) the right to live, work, and study in Spain. The primary requirement is purchasing real estate worth at least €500,000. The property can be residential or commercial, and you can combine multiple properties to meet the threshold (e.g., two apartments worth €250,000 each). The Golden Visa is renewable every two years initially, then every five years, and after 10 years of continuous residence, you can apply for permanent residency or Spanish citizenship. Importantly, the Golden Visa does not require you to live in Spain full-time—you need only visit once per year to maintain your status, making it ideal for buyers seeking flexibility.

Non-lucrative visa Spain: This is the most popular route for retirees and financially independent individuals who do not plan to work in Spain. You must demonstrate sufficient passive income (pensions, dividends, rental income from other countries) to support yourself without employment—currently around €28,000 per year for a single applicant, plus approximately €7,000 per additional family member. You must also prove you have medical insurance and clean criminal records. Unlike the Golden Visa, the Non-Lucrative Visa requires you to spend at least 183 days per year physically present in Spain (making you a tax resident), and it prohibits paid employment. However, it is renewable annually for two years, then for two-year periods, and leads to permanent residency after five years.

Digital Nomad Visa: Launched in 2023, this visa targets remote workers, freelancers, and employees of non-Spanish companies who can work from anywhere. You must prove that at least 80% of your income comes from clients or employers outside Spain, demonstrate stable monthly income (typically around €2,000–€2,500 per month), and show proof of remote work arrangements. The visa is granted for one year initially and renewable for up to five years. It allows you to live in Spain while maintaining your existing job or freelance business, making it ideal for younger buyers seeking lifestyle flexibility.

Family Reunification Visa: If you have immediate family members who are already Spanish residents or citizens, you can apply to join them. This route is particularly relevant for buyers whose adult children or spouses already live in Spain.

Work Visa / Self-Employment Visa: If you plan to Starting business in Spain or secure employment with a Spanish company, you can apply for a work visa or an entrepreneur visa, both of which lead to residency.

For detailed step-by-step application processes and documentation checklists for each visa type, see Spanish visas and residency in Spain.

Can I Get Permanent Residency in Spain if I Buy a House?

Buying a house alone does not grant you permanent residency, but it can facilitate the path to it via the Golden Visa route. If you purchase property worth €500,000 or more and obtain a Golden Visa, you can renew that visa indefinitely as long as you maintain your investment and visit Spain at least once per year. After five years of continuous legal residence in Spain (meaning you have held valid residency authorization for five consecutive years), you become eligible to apply for permanent residency, which no longer requires you to maintain the €500,000 investment. Permanent residency grants you the same rights as Spanish citizens except voting in national elections, and after 10 years of legal residence, you can apply for Spanish citizenship and a passport. Note that the Golden Visa's minimal physical presence requirement (one visit per year) does not count toward the residency time needed for citizenship; if your goal is naturalization, you must spend at least 183 days per year in Spain to demonstrate genuine integration.

Lawyer's Insight: Many buyers mistakenly believe that the Golden Visa automatically leads to permanent residency after five years. It does not. You must actively apply for permanent residency when you become eligible, providing updated proof of income, health insurance, and clean criminal records. If you fail to renew your Golden Visa or allow it to lapse, your residency status is immediately revoked, and you revert to the 90-day tourist rule. Always work with a qualified immigration lawyer to ensure your renewals are submitted on time and all documentation is accurate. For post-Brexit residency planning, see living in Spain after Brexit.

3. Where to Buy and Market Trends

Spain's diverse geography offers buyers an extraordinary range of climates, property types, and price points—from the sun-drenched beaches of the Costa del Sol to the cooler, greener hills of Galicia, and from the cosmopolitan energy of Barcelona to the island tranquility of the Balearics. However, regional choice is about far more than lifestyle preference; it directly impacts your tax liability (transfer taxes vary by autonomous community), rental yield potential, resale liquidity, and even legal risk. This section strips away generic travel descriptions and focuses on the hard data: which markets are appreciating, where foreign buyers concentrate, and the specific legal pitfalls associated with rural, off-plan, and island properties.

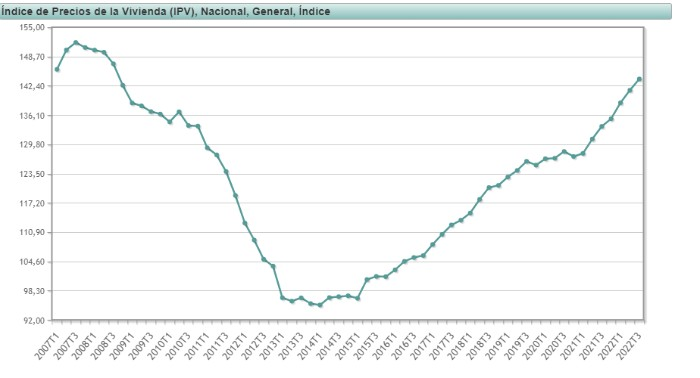

Market Recovery and Current Price Trends

The Spanish National Institute of Statistics (INE) provides a graph showing the evolution of average property prices (in thousands of Euros) from 2007 to Q3 2022:

Chart: Spanish property price change from 2007 to 2022, illustrating near-complete recovery to pre-financial-crisis levels.

Property values have nearly recovered to pre-2007/8 financial crisis levels, but regional variations exist, influenced by factors like beach proximity, city centre location, and property style and age. Coastal and island markets—particularly the Balearics, Costa del Sol, and Canary Islands—have outpaced the national average, driven by limited supply, high foreign demand, and strong short-term rental yields. Inland regions such as Extremadura and Castilla-La Mancha remain significantly below 2007 peaks, offering value opportunities for buyers prioritizing affordability over rental income.

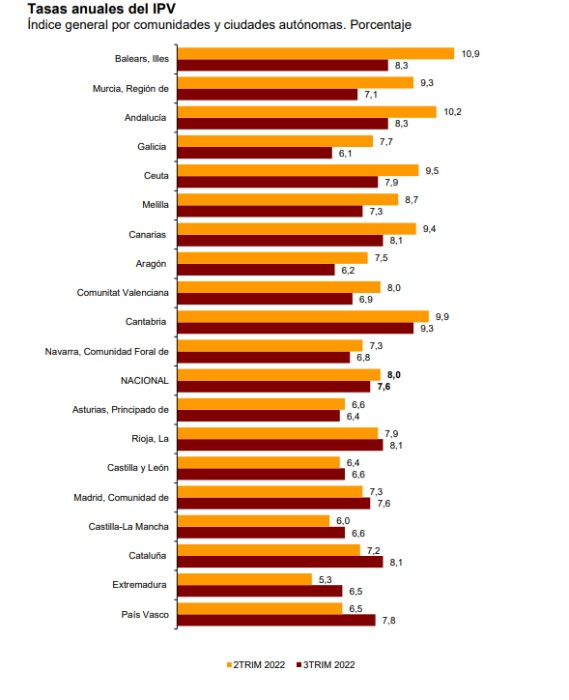

Recent figures from the Land Registries Association show a slowing rate of price increases in most Autonomous Communities, with Q2 2022 seeing slower growth compared to Q3 2021:

Chart: Spanish property value changes between Q2 and Q3 2022, showing a market slowdown as interest rates began rising.

With rising interest rates, if you need a mortgage, act quickly to secure a sufficient loan. Cash buyers might prefer to watch market trends over the coming months, as the combination of higher borrowing costs and slowing price growth could create negotiation leverage. For updated market statistics, see the Land Registries Association of Spain.

Image: Popular regions for UK and international buyers, from coastal resorts to emerging northern markets.

Regional Considerations for Foreign Buyers

Spain offers a huge range of buying opportunities for British and other foreign citizens, with each region offering unique advantages in climate, geography, property types, and prices. However, some regions present higher legal risk than others:

The Balearic Islands (Mallorca, Ibiza, Menorca, Formentera) remain the most expensive markets in Spain, with median prices frequently exceeding €4,000 per square meter in prime coastal areas. Transfer tax rates are also the highest in Spain, reaching up to 13% for properties over €2 million. Buyers should budget accordingly.

The Canary Islands (Gran Canaria, Lanzarote, Tenerife, Fuerteventura) offer year-round subtropical climate and lower transfer taxes (6.5%, the lowest in Spain), making them attractive for buy-to-let investors. However, many Canary Island properties—especially in rural and semi-rural areas—suffer from irregular planning permissions and incomplete legal documentation.

Galicia in the northwest has emerged as a surprise favorite among Northern European buyers seeking cooler, greener climates as a result of climate change and increased heat in more southern latitudes. Prices remain well below national averages, but rural properties often lack proper land registry documentation.

Barcelona and Valencia offer strong rental yields due to high demand from students, expats, and tourists, but both cities have introduced strict short-term rental licensing regimes that can make Airbnb-style lettings illegal without proper permits.

Image: Regional diversity in Spanish property markets, from traditional inland culture to modern coastal developments.

For more in-depth information, see our guide: Discover the best places to buy in Spain.

Image: The breadth of property options available to international buyers, from rural fincas to urban apartments.

Legal Pitfalls: Off-Plan and Rural Properties

⚠️ Legal Warning: Flaws in Building License or Planning Permissions. When buying land in Spain or purchasing off-plan properties (those not yet constructed), extreme caution is required. Many developments—especially in rural or semi-rural areas—lack proper building licenses (licencia de obra) or have been constructed in violation of local planning codes. If a property is built without proper permits, local authorities can order its demolition, and you will have no legal recourse to recover your investment.

This is particularly common in the Canary Islands, Andalusia, and rural Catalonia. Always instruct your lawyers in Spain to obtain a certificate from the local town hall (Ayuntamiento) confirming that the property has a valid licencia de primera ocupación (first occupation license) before signing any contracts. Off-plan purchases also carry the risk of developer insolvency; Spanish law requires developers to provide bank guarantees for advance payments, but enforcement is inconsistent. Never transfer money directly to a developer—always use an independent escrow account managed by your lawyer.

4. The Costs & Taxes of Buying Property in Spain

One of the most common sources of buyer shock when purchasing Spanish property is the realization that the purchase price is only the starting point. The total cost of buying property in Spain includes more than just the purchase price. Buyers should consider property transfer tax, notary costs, land registry fees, legal fees, and potential estate agent commissions. These additional expenses typically add 10% to 15% on top of the headline purchase price, and failing to budget for them can derail your financing plans or force you to reduce your property budget significantly. This section provides exact figures and official fee tables to help you calculate your total acquisition cost down to the euro.

What Taxes Do I Pay When Buying a Property in Spain?

The biggest tax when buying property in Spain is either IVA (VAT) or ITP (transfer tax), depending on whether the property is new or resale:

New Properties: The purchase of a new property in Spain currently attracts a VAT rate (IVA) of 10% of the property purchase price. "New" is defined as any property being sold for the first time by a developer or builder, including off-plan properties and recently completed developments. In addition to the 10% IVA, you must also pay AJD (Stamp Duty), which ranges from 0.5% to 1.5% depending on the autonomous community. For example, in Catalonia, AJD is 1.5%, while in Madrid it is 0.75%. This means the total tax cost for a new property ranges from 10.5% to 11.5%.

Resale Properties: The purchase of a resale property in Spain attracts ITP or transfer tax, which varies across Spain but is typically between 7% and 11% of the purchase price. Unlike IVA, there is no additional stamp duty on resale purchases. The exact ITP rate depends on the autonomous community and, in some regions, the value of the property. For example:

- Canary Islands: 6.5% (the lowest in Spain)

- Madrid: 6% (flat rate)

- Catalonia: 10% for properties up to €1 million, 11% above that

- Balearic Islands: 8% for properties up to €400,000, scaling up to 13% for properties over €2 million

Example Calculation (Resale Property in Valencia):

- Purchase price: €300,000

- ITP (10%): €30,000

- Notary fees (approx.): €800

- Land registry fees (approx.): €400

- Legal fees (approx. 1% + VAT): €3,630

- Surveyor (optional but recommended): €500–€1,000

- Total acquisition cost: approximately €335,000–€336,000

What Fees Are There When Buying a House in Spain?

In addition to transfer taxes, you will pay the following professional and administrative fees:

Notary Fees: The notary (notario) is a state-appointed official who witnesses and legalizes the sale contract. Notary fees are set by law and are based on the purchase price of the property. The Association of Spanish Notaries publishes the official fee scale, which ranges from approximately €600 for a €100,000 property to €850 for a €300,000 property. These are approximate figures; the exact amount will be calculated by the notary and stated on your completion statement.

Land Registry Fees: After the notary signing, your lawyer will register the property in your name at the local Land Registry (Registro de la Propiedad). Registry fees are also fixed by law and vary by property value. Below is the official fee table for registry costs:

| Cost of the Property | Registry Costs |

|---|---|

| €25,000 | €295 |

| €50,000 | €230 |

| €100,000 | €345 |

| €150,000 | €370 |

| €200,000 | €395 |

| €300,000 | €445 |

| €400,000 | €495 |

| €500,000 | €545 |

Legal Fees: Hiring an independent lawyer is not legally mandatory in Spain, but it is universally recommended by all legal professionals. Your lawyer will conduct due diligence checks on the property (verifying title, checking for debts, confirming planning permissions), draft or review contracts, handle the transfer of funds, and attend the notary signing on your behalf. Legal fees typically range from 1% to 1.5% of the purchase price plus VAT (21%), meaning you should budget approximately €1,210 to €1,815 per €100,000 of purchase price. This is money well spent; a competent lawyer can save you tens of thousands of euros by identifying title defects, tax overpayments, or undisclosed debts before you commit to the purchase.

Surveyor Fees: While not legally required, a structural survey is highly recommended, especially for older properties or rural buildings. Surveyor fees range from €500 to €1,500 depending on the size and complexity of the property. Surveys can uncover serious defects such as aluminosis (a structural defect caused by aluminum-contaminated concrete common in buildings from the 1960s and 1970s), subsidence, damp, or illegal extensions that could result in demolition orders.

Estate Agent Fees: In Spain, estate agent commissions are almost always paid by the seller, not the buyer. However, some agents attempt to charge both parties, particularly in high-demand markets. Always clarify in writing whether you are expected to pay any commission before signing an agency agreement.

Worked Examples: How Much Tax Do You Pay on Buying a Property in Spain?

To summarize the total tax burden:

For a €200,000 resale property in Madrid:

- ITP (6%): €12,000

- Notary: ~€700

- Land Registry: €395

- Legal fees (1% + VAT): ~€2,420

- Total tax and fees: approximately €15,515 (7.8% of purchase price)

For a €200,000 new property in Catalonia:

- IVA (10%): €20,000

- AJD (1.5%): €3,000

- Notary: ~€700

- Land Registry: €395

- Legal fees (1% + VAT): ~€2,420

- Total tax and fees: approximately €26,515 (13.3% of purchase price)

Lawyer's Insight: Many buyers are shocked to discover that new properties carry significantly higher tax costs than resale properties due to the combination of IVA and stamp duty. This is one reason why resale properties often represent better value for foreign buyers, particularly in markets where new-build supply is limited and priced at a premium. Always request a detailed breakdown of all costs from your lawyer before making an offer, and ensure your financing arrangements account for these additional expenses.

Do I Pay Annual Taxes if I Buy a House in Spain?

Yes—the taxes described above are unavoidable. However, there are ongoing annual taxes you must also budget for:

IBI (Council Tax): All property owners must pay annual municipal property tax, ranging from 0.4% to 1.1% of the cadastral value. For a property with a cadastral value of €100,000, expect to pay €400–€1,100 per year.

Non-Resident Income Tax: If you do not live in Spain full-time If you do not live in Spain full‑time, you must pay non‑resident income tax each year on your Spanish property, even if you never rent it out. The tax is calculated on an imputed rental value based on the cadastral value, at 19% for EU/EEA residents and 24% for non‑EU owners such as UK or US nationals. If you do rent the property, you will also pay income tax on actual rental earnings, with EU/EEA owners able to deduct certain expenses, while non‑EU owners generally cannot.

5. The Costs & Taxes of Buying Property in Spain

Understanding the full financial picture is essential before committing to a Spanish property purchase. The purchase price is just the beginning—buyers must budget for multiple taxes, legal fees, and administrative costs that can add 10–15% to the total investment. Failing to budget for these items can derail your financing plans or force you to reduce your property budget significantly.

The biggest variable cost is property transfer tax, which depends on whether you're buying new or resale. The purchase of a new property in Spain currently attracts a VAT rate of 10% of the property purchase price, known locally as IVA (Impuesto sobre el Valor Añadido). In the Canary Islands, this rate drops to 7% under their regional IGIC system. Additionally, new property purchases incur a stamp duty called AJD (Actos Jurídicos Documentados), typically 1–1.5% of the purchase price.

The purchase of a resale property in Spain attracts ITP or transfer tax, which varies across Spain but is typically between 7% and 11% of the purchase price. The exact rate depends on the autonomous region and sometimes the property value. For example, the Canary Islands charge 6.5%, while the Balearic Islands can charge up to 13% for properties exceeding €2 million. Catalonia and Valencia typically apply 10%, while Andalusia charges 7–10% depending on the declared value.

Beyond transfer taxes, buyers face several mandatory professional fees. Notary fees are regulated by law and typically range from €600 to €1,200 depending on property value. Land Registry inscription costs follow a similar sliding scale. Legal fees for an independent lawyer typically run 1–1.5% of the purchase price plus IVA, while surveyor fees generally cost €300–600 for a standard residential property. The Association of Spanish Notaries provides official fee schedules updated annually.

What taxes and fees apply when buying property in Spain?

The primary taxes depend on whether the property is new construction or resale. New properties incur 10% IVA (VAT) on the purchase price plus 1–1.5% AJD stamp duty, so you should expect a total tax burden of roughly 11–11.5% on top of the agreed price. Resale properties are subject to ITP (transfer tax) only, ranging from 6.5% to 13% depending on your autonomous region and property value tier.

By way of illustration, typical ITP ranges include 6.5% in the Canary Islands (the lowest in Spain), 6% in Madrid, 10% in Catalonia and Valencia (rising to 11% for high‑value properties in Catalonia), and a progressive 8–13% scale in the Balearic Islands for more expensive homes. In addition, all buyers—new or resale—must budget for notary fees (€600–€1,200), Land Registry fees (€300–€700), and legal fees (typically 1–1.5% of purchase price plus 21% IVA). If you're financing the purchase, add mortgage‑related AJD of approximately 1–1.5% on the loan amount.

Example (Resale Property in Valencia):

- Purchase price: €300,000

- ITP (10%): €30,000

- Notary fees (approx.): €800

- Land Registry fees (approx.): €400

- Legal fees (approx. 1% + VAT): €3,630

- Surveyor (optional but recommended): €500–€1,000

- Total acquisition cost: approximately €335,000–€336,000

Lawyer's Insight: Many foreign buyers mistakenly budget only for the headline ITP or IVA rate and are shocked when closing costs exceed their estimates by €10,000–€15,000. As a rule of thumb, always add a 12–15% buffer above the purchase price for total acquisition costs to avoid last‑minute financing gaps.

What other buying costs should I budget for in Spain?

In addition to the purchase taxes described above, you will pay several professional and administrative fees that are effectively unavoidable if you want a safe transaction.

Notary Fees: The notary (notario) is a state‑appointed official who witnesses and legalizes the sale contract. Notary fees are set by law and are based on the purchase price of the property. The Association of Spanish Notaries publishes the official fee scale, which ranges from approximately €600 for a €100,000 property to €850 for a €300,000 property. These are approximate figures; the exact amount will be calculated by the notary and stated on your completion statement.

Land Registry Fees: After the notary signing, your lawyer will register the property in your name at the local Land Registry (Registro de la Propiedad). Registry fees are also fixed by law and vary by property value. Below is the official fee table for registry costs:

| Cost of the Property | Registry Costs |

|---|---|

| €25,000 | €295 |

| €50,000 | €230 |

| €100,000 | €345 |

| €150,000 | €370 |

| €200,000 | €395 |

| €300,000 | €445 |

| €400,000 | €495 |

| €500,000 | €545 |

Legal Fees: Hiring an independent lawyer is not legally mandatory in Spain, but it is universally recommended by all legal professionals. Your lawyer will conduct due diligence checks on the property (verifying title, checking for debts, confirming planning permissions), draft or review contracts, handle the transfer of funds, and attend the notary signing on your behalf. Legal fees typically range from 1% to 1.5% of the purchase price plus VAT (21%), meaning you should budget approximately €1,210 to €1,815 per €100,000 of purchase price.

Surveyor Fees: While not legally required, a structural survey is highly recommended, especially for older properties or rural buildings. Surveyor fees range from €500 to €1,500 depending on the size and complexity of the property and can uncover serious defects such as aluminosis, subsidence, damp, or illegal extensions that could result in demolition orders.

Other common costs: Estate agent commissions (normally paid by the seller, but always confirm in writing), NIE application fees (€10–€15, or €50–€100 via a gestor), mortgage arrangement fees (0.5–1% of loan value), bank account setup fees, and translation services (€100–€300 for certified translations). According to data from the Land Registries Association of Spain, the average total transaction costs (excluding the purchase price) for foreign buyers in 2023 ranged from €15,000 to €25,000 for properties valued at €200,000–€300,000.

Worked examples: how much tax and fees do you actually pay?

To put these figures into context, here are two typical purchase scenarios:

For a €200,000 resale property in Madrid:

- ITP (6%): €12,000

- Notary: ~€700

- Land Registry: €395

- Legal fees (1% + VAT): ~€2,420

- Total tax and fees: approximately €15,515 (7.8% of purchase price)

For a €200,000 new property in Catalonia:

- IVA (10%): €20,000

- AJD (1.5%): €3,000

- Notary: ~€700

- Land Registry: €395

- Legal fees (1% + VAT): ~€2,420

- Total tax and fees: approximately €26,515 (13.3% of purchase price)

Lawyer's Insight: New properties often carry significantly higher tax costs than resale properties due to the combination of IVA and AJD. This is one reason why resale properties frequently represent better overall value for foreign buyers, particularly in markets where new‑build supply is limited and priced at a premium.

What ongoing property taxes will I pay each year?

Yes—the purchase taxes described above are one‑off, but there are ongoing annual taxes you must also budget for once you own the property.

IBI (Council Tax): All property owners must pay annual municipal property tax, ranging from 0.4% to 1.1% of the cadastral value. For a property with a cadastral value of €100,000, expect to pay €400–€1,100 per year in IBI.

Non‑Resident Income Tax: If you do not live in Spain full‑time, you must pay non‑resident income tax each year on your Spanish property, even if you never rent it out. The tax is calculated on an imputed rental value based on the cadastral value, at 19% for EU/EEA residents and 24% for non‑EU owners such as UK or US nationals. If you do rent the property, you will also pay income tax on actual rental earnings, with EU/EEA owners able to deduct certain expenses, while non‑EU owners generally cannot.

⚠️ Legal Warning: The cadastral value (official tax valuation) and the purchase price you negotiate are not always the same. Spanish tax authorities can challenge transactions where the declared price appears artificially low, potentially triggering audits, reassessment using their own reference values, and penalties. Always declare a realistic market value and ask your lawyer to verify the fiscal value used for tax calculations.

⚠️ Legal Warning: The Catastral value (official tax valuation) and the purchase price you negotiate are not always the same. Spanish tax authorities can challenge transactions where the declared price appears artificially low, potentially triggering audits and penalties. Always declare the true market value.

6. Financing Your Spanish Property

Securing financing as a foreign buyer requires careful planning and realistic expectations. While Spanish mortgages for non-residents are available, lending criteria differ significantly from domestic mortgages, and interest rates reflect the higher risk profile banks assign to international clients.

The buyer will need to have sufficient funds to cover a deposit of at least 30% for non-residents, compared to 20% for Spanish residents. Most Spanish banks will lend up to 70% loan-to-value (LTV) for non-resident buyers, though this can drop to 60% for older properties or rural locations. EU citizens generally secure better terms than non-EU nationals, with interest rates in early 2025 averaging 4-4.5% for non-residents versus 3.5-4% for residents.

According to the Bank of Spain, average mortgage interest rates for terms over three years slightly eased in early 2024, dropping to just below 4%. However, non-residents typically pay a 0.5-1% premium above these reference rates, and many Spanish banks have tightened lending criteria post-2023 due to European Central Bank rate adjustments.

Beyond the deposit, mortgage applicants must demonstrate stable income—usually requiring proof of earnings at least 3-4 times the annual mortgage payment. Spanish banks scrutinize foreign income sources carefully, often requesting translated bank statements, tax returns, and employer references. Processing timelines for non-resident mortgages typically run 6-8 weeks, considerably longer than domestic applications.

Do I need a Spanish bank account to buy a property in Spain?

While not strictly a legal requirement, a Spanish bank account is practically essential for property purchase and ownership. You cannot pay the notary or seller directly in cash for amounts exceeding €1,000 under Spanish anti-money-laundering regulations, and international wire transfers for large property purchases trigger extensive documentation requirements that delay completion.

More importantly, ongoing property ownership requires local payment infrastructure. You'll need to set up direct debits for utilities (electricity, water, internet), community fees, annual property taxes like Council Tax in Spain (IBI), and potentially rental income collection if you plan to let the property. Most Spanish utility companies and community administrators do not accept foreign bank accounts for automatic payments.

Opening a bank account in Spain as a non-resident requires your NIE number, passport, proof of address (from your home country), and sometimes a minimum deposit of €500-€1,000. Major banks like Santander, CaixaBank, and Sabadell offer dedicated non-resident account services, though monthly maintenance fees typically run €10-€20 unless you maintain minimum balances.

How much money do you need for a mortgage in Spain?

Non-residents can get a mortgage in Spain, but lenders require substantially larger deposits than domestic buyers. The buyer will need to have sufficient funds to cover a deposit (typically) of at least 30% of the purchase price, compared to 20% for Spanish residents.

For a €200,000 property:

- Minimum deposit: €60,000 (30%)

- Maximum mortgage: €140,000 (70% LTV)

- Additional closing costs: €20,000-€25,000

- Total cash required: €80,000-€85,000

Banks also assess your income-to-debt ratio rigorously. Most require that your total monthly debt obligations (including the new Spanish mortgage) do not exceed 35-40% of your gross monthly income. For a €140,000 mortgage over 20 years at 4.5%, expect monthly payments around €900—requiring documented income of at least €2,500-€3,000 per month.

Lawyer's Insight: US and Canadian citizens face additional hurdles due to FATCA (Foreign Account Tax Compliance Act) reporting requirements, which make some Spanish banks reluctant to lend to North American buyers. If you're financing as a US citizen, start the mortgage application process 3-4 months before your planned purchase date.

Is it possible to mortgage a house in Spain as a US citizen?

Yes, but US citizens face additional documentation and compliance requirements that complicate the process. Spanish banks must comply with FATCA regulations, which require them to report account details and loan information for US taxpayers to the IRS. This administrative burden makes some smaller banks and cajas (regional savings banks) reluctant to work with American buyers.

Larger international banks like Santander, BBVA, and Sabadell have established FATCA-compliant processes and actively serve US citizen clients. However, expect to provide additional documentation including US tax returns (typically 2-3 years), IRS Form W-9, proof of US tax compliance, and potentially a letter from your US bank confirming your financial standing.

Interest rates for US citizens typically run 0.25-0.5% higher than EU non-residents due to perceived exchange rate and documentation risks. Most Spanish banks also require US buyers to maintain the property insurance policy and provide annual proof of tax in Spain compliance. Budget an extra 2-3 weeks in your purchase timeline specifically for FATCA documentation review.

Which Spanish bank is best for non-residents?

Several Spanish banks have developed strong non-resident services, though "best" depends on your specific circumstances—citizenship, purchase location, and whether you need mortgage financing or just transaction banking.

Top banks for non-resident property buyers:

Santander: Largest Spanish bank with extensive English-language support and offices throughout expat-heavy regions like Costa del Sol and Costa Blanca. Offers competitive mortgage rates for non-residents (typically 4-4.5%) and has streamlined FATCA processes for US citizens. Monthly account fees: €10-€15 with waiver for minimum balance.

CaixaBank: Strong presence in Catalonia, Valencia, and the Balearic Islands. Known for efficient mortgage processing (4-6 weeks) and flexible income verification for self-employed buyers. Provides dedicated non-resident account managers. Monthly fees: €12-€18.

Sabadell: Particularly strong for UK and Irish buyers, with Brexit-specific documentation support. Offers combined mortgage-and-account packages that reduce overall fees. Has English-speaking staff in most coastal branches. Monthly fees: €8-€12.

BBVA: Best for Latin American buyers due to its extensive network in Mexico, Colombia, and Argentina. Efficient at verifying foreign income sources from these markets. Monthly fees: €10-€15.

Most banks waive monthly fees if you maintain a minimum balance (typically €3,000-€5,000) or set up regular direct debits. All require your Spanish NIE number to open a non-resident account, so prioritize obtaining this before approaching banks.

7. The Step-by-Step Legal Purchase Process

Navigating the legal purchase process requires careful coordination between multiple parties—your lawyer, the seller's representatives, notary, Land Registry, and your bank. Understanding this sequence helps you anticipate requirements and avoid costly delays that can jeopardize your purchase timeline or deposit.

In 2023—the last full year for which we have statistics—more than 87,000 properties were purchased in Spain by foreign buyers. This represented 15% of the total number of conveyances that took place, up from 13.7% the previous year. These figures demonstrate that despite living in Spain after Brexit concerns and global economic uncertainty, the Spanish property market remains highly accessible to international buyers who follow proper legal procedures.

The process generally takes 8-12 weeks from initial offer to completion, though this varies considerably based on whether you're purchasing with cash or require mortgage approval. Properties with complex title issues, rural properties requiring additional licenses, or transactions involving inheritance can extend this timeline to 4-6 months. Your lawyer's due diligence work occurs simultaneously with your mortgage application (if applicable), making the choice of experienced lawyers in Spain critical to maintaining momentum.

What are the requirements to buy a property in Spain?

Before being able to do, well almost anything in Spain (and certainly to purchase a property) you will need to get a Spanish NIE number—a foreigner identification number. This unique identifier is absolutely mandatory for property transactions, opening bank accounts, signing utility contracts, and paying taxes.

Core requirements for property purchase:

- NIE number: Apply at Spanish consulate in your home country (2-4 weeks) or in Spain with your lawyer's assistance (1-2 weeks)

- Spanish bank account: Required for fund transfers and ongoing property expenses

- Proof of funds: Bank statements showing sufficient capital for deposit, purchase price, and closing costs

- Passport: Valid for at least 6 months beyond purchase date

- Independent legal representation: While not legally mandatory, securing good legal advice ensures a smooth process and safeguards your property investment

Your lawyer will carry out initial due diligence checks to make sure licenses, title deeds, and Land Registry records are in place and match the property being sold. This typically involves requesting a Nota Simple (Land Registry extract), reviewing the Catastral records, checking for outstanding debts or liens, and verifying building licenses for any renovations or extensions.

⚠️ Legal Warning: Some sellers or agents may pressure you to proceed without independent legal representation to "save costs" or "speed up the process." This is a red flag. The notary in Spain is a neutral state official who verifies the legality of the transaction—they do NOT represent your interests or check for problems that could cost you thousands.

Do I need a lawyer to buy property in Spain?

Technically, Spanish law does not mandate that buyers hire their own independent lawyer—only that the transaction be formalized before a notary. However, this represents one of the most dangerous misconceptions in Spanish property purchasing. The notary is a public official who verifies identities, confirms the legal capacity of parties, and ensures the deed complies with Spanish law. They do NOT investigate title defects, verify building permissions, check for hidden debts, or protect your interests against the seller.

Securing good legal advice ensures a smooth process and safeguards your property investment in several critical ways. Your lawyer will carry out initial due diligence checks to make sure licenses, title deeds, and registry records are in place. This includes requesting a Nota Simple from the Land Registry to verify ownership and identify any mortgages, liens, or embargoes (embargos) attached to the property. They'll also cross-reference the Catastral registry to ensure the property description, boundaries, and declared square meters match reality.

Real-World Example: In 2022, we represented a UK buyer who found a "bargain" Costa Blanca villa listed at €180,000—approximately €60,000 below market value. Initial excitement turned to alarm when our due diligence revealed the property had an illegal pool extension built without a license, which would cost €25,000 to legalize, plus potential municipal fines of €15,000-€30,000. Without a lawyer, the buyer would have inherited this €40,000-€55,000 liability without recourse.

Beyond due diligence, your lawyer manages the deposit process, drafts or reviews the arras (reservation) contract to protect your deposit if the seller breaches, coordinates with your mortgage bank, calculates exact tax obligations, and represents you at the notary signing if you cannot attend in person through a Power of Attorney.

Legal fees typically run 1-1.5% of the purchase price plus 21% IVA—a €2,500-€3,500 investment on a €200,000 property that can easily save you €20,000-€50,000 in avoided problems. For comprehensive guidance on your obligations, review our detailed article on Spanish Property Laws.

Can I open a Spanish bank account with NIE?

Yes—your NIE number is the primary document Spanish banks require to open a non-resident account. Without it, banks cannot legally establish your account, as they must register your fiscal identification with Spanish tax authorities for future reporting obligations.

Documents required for non-resident account opening:

- Valid passport

- NIE certificate (original or certified copy)

- Proof of address from your home country (utility bill, bank statement dated within 3 months)

- Initial deposit (varies by bank, typically €500-€1,000)

- Employment letter or proof of income (some banks require this)

An NIE may also be arranged by your legal representative using a Power of Attorney if you cannot travel to Spain for the appointment, though this adds €100-€200 in notarization and legalization fees. Most lawyers in Spain offer NIE application services for €150-€300, handling the appointment booking, form completion, and document collection on your behalf.

Processing timelines at Spanish banks have improved significantly since 2020. Most major banks can open non-resident accounts within 5-10 business days once you provide complete documentation, though some require an in-person branch visit for identity verification. Mobile banking apps and online English-language interfaces are now standard at Santander, CaixaBank, BBVA, and Sabadell. For detailed guidance, see our complete article on opening a bank account in Spain.

What to know before buying a house in Spain?

Understanding common pitfalls can save you from making a costly mistake. Spanish property law differs significantly from common-law systems in the UK, US, and Canada, and certain problems that would be obvious red flags in your home country may not be immediately apparent in Spanish transactions.

Potential Pitfall: Problems with Title

When buying Spanish property, ensure it is registered in the Land Registry, as unregistered properties—while often put up for sale to unsuspecting foreign buyers—can result in worthless investments. Additionally, verify that the details match the Catastro register, managed by the Tax Agency, to avoid registration issues and potential tax overpayments. Some rural properties and older coastal properties in regions like Andalusia and Galicia remain unregistered despite being occupied for decades. Without formal Land Registry inscription, you cannot prove legal ownership, cannot obtain a mortgage, and will face immense difficulty selling the property in future.

Your lawyer should always obtain and review the Nota Simple before you commit to any deposit. This official Land Registry document reveals the registered owner, property boundaries, square meters, any mortgages or liens, and legal restrictions. If the property is not registered, or if the registered owner doesn't match the seller, walk away immediately or require the seller to resolve the issue before proceeding.

Potential Pitfall: Construction Errors

Before buying Spanish property, a survey is essential. Issues like aluminosis, caused by adding aluminum to concrete in the 1960s and 1970s, can make buildings unstable and unhealthy, especially in humid coastal areas. Local lawyers and surveyors can identify such problems, explaining why a property might seem like a bargain. This defect primarily affects properties built between 1960-1980 in Catalonia, Valencia, and the Balearic Islands.

Other common structural issues include inadequate foundation work on hillside properties (leading to subsidence), outdated electrical systems that don't meet current safety codes, and hidden water damage from roof leaks or poor drainage. A professional survey costs €300-€600 but can reveal €20,000-€50,000 in necessary repairs—critical information for price negotiation or deciding to withdraw from the purchase.

Potential Pitfall: Flaws in License

Properties, especially new developments or rural homes, may lack proper building licenses or Certificado de Habitabilidad (Certificate of Habitability), which confirms the property meets minimum health and safety standards for occupation. Without this certificate, you cannot register utilities in your name, cannot obtain residency using this address, and may face municipal fines.

Off-plan purchases and rural properties converted from agricultural use are particularly high-risk. Always verify that the developer or previous owner obtained a Licencia de Primera Ocupación (First Occupation License) before the property was sold. If buying land to build, ensure the plot has building permission—not all land parcels in Spain are legally buildable. For comprehensive guidance, see our guide to buying land in Spain.

Potential Pitfall: Unexpected Costs

Be careful as there is a risk of substantial costs beyond the purchase price that many foreign buyers fail to anticipate. These include outstanding community fees (gastos de comunidad) that transfer to the new owner if unpaid by the seller, IBI property taxes for the current year (often split proportionally), connection fees for utilities if they've been disconnected, and mandatory property insurance.

Community fees for apartments and townhouses in managed developments typically run €50-€200 per month depending on shared amenities (pools, gardens, security). Your lawyer should request a certificate from the community (Certificado de Comunidad) proving the seller has paid all fees to date—otherwise, you inherit this debt automatically under Spanish law. Similarly, verify that the seller has paid IBI through the current calendar year, as town halls can pursue the new owner for unpaid property taxes from previous years.

Want to hear what other clients

are saying about us?

8. Frequently Asked Questions

How long is the house buying process in Spain?

The typical Spanish property purchase takes 8-12 weeks from initial offer to final notary signing and key handover, though timelines vary significantly based on payment method and property complexity.

Cash buyers can often complete within 4-6 weeks if all legal documentation is in order. This timeline assumes: 1 week for offer acceptance and reservation contract, 2-3 weeks for lawyer's due diligence (Nota Simple, Catastral checks, license verification), 1 week for fund transfer and tax calculation, and 1-2 weeks for notary appointment scheduling and deed signing.

Mortgage buyers typically require 10-14 weeks due to bank processing timelines. Spanish banks need 6-8 weeks to process non-resident mortgage applications, conduct property valuations, and issue formal loan offers. This mortgage timeline runs parallel to legal due diligence but often becomes the critical path determining completion date.

Properties with title defects, unclear boundaries, inheritance issues, or missing building licenses can extend timelines to 4-6 months while sellers resolve problems. Rural properties and older coastal homes frequently fall into this category, making pre-purchase research critical to realistic timeline planning.

Can I gift my house in Spain to my son?

Yes, you can gift property in Spain to your son, but the transaction triggers significant tax obligations for the recipient that often surprise families. Unlike some countries where gifts between close family members receive favorable treatment, Spain applies inheritance tax in Spain rates to lifetime gifts, which vary dramatically by autonomous region and relationship.

The recipient pays gift tax at rates ranging from 7.65% to 34% of the property's Catastral value, depending on the region and total gift value. Immediate family (children, spouses) receive allowances and reductions in most regions, but these vary: Andalusia offers generous allowances of up to €250,000 for children, while Catalonia applies relatively high rates even for direct descendants.

Additionally, the donor may face capital gains tax liability if the property has appreciated since purchase. Spanish tax authorities calculate capital gains based on the difference between your original purchase price (adjusted for inflation) and the current market value at gift date, taxing this gain at 19-26% depending on the amount. This makes gifting potentially more expensive than inheritance in many cases.

Lawyer's Insight: Many expats are better served by retaining property ownership and using Spanish Wills to pass property on death, which may qualify for larger tax allowances. Always model both scenarios with a tax specialist before proceeding with lifetime gifts, as the tax difference can easily reach €20,000-€40,000 for a €200,000 property.

How much money do I need in the bank to retire to Spain?

Spain's non-lucrative visa—the primary route for retirees without Spanish work plans—requires proof of substantial passive income or savings to ensure you won't become a burden on Spanish social services. The current financial requirements for 2026 are calculated as 400% of Spain's IPREM (Public Income Indicator) for the principal applicant, plus 100% IPREM for each dependent.

For 2026, this translates to approximately €28,800 per year for a single person, or €2,400 per month. For couples, add approximately €7,200 per year (€600/month) for the spouse. These funds must be demonstrated through a combination of pension income, investment income, rental income, or liquid savings. If relying on savings rather than recurring income, Spanish consulates typically require proof of at least €50,000-€75,000 in accessible funds for a single applicant.

You must also provide proof of Spanish private medical insurance coverage (approximately €1,200-€2,000 per year for applicants over age 65) and a clean criminal record. The visa allows residency but prohibits employment in Spain, making it suitable for genuinely retired individuals or those with location-independent passive income. For complete guidance, see our detailed article on Retirement in Spain.

How much money do I need to get residency in Spain?

Residency requirements vary dramatically depending on which visa category you qualify for. The Golden Visa Spain requires a property investment of at least €500,000, making it the most capital-intensive but also the most flexible option, as it allows visa-free travel throughout the Schengen Zone and does not require you to spend minimum time in Spain annually.

The Non-lucrative visa Spain requires approximately €28,800 per year in passive income or equivalent savings (roughly €50,000-€75,000 in liquid assets), but prohibits employment in Spain. This suits retirees or individuals with substantial investment income.

The Digital Nomad Visa requires proof of remote employment or self-employment generating at least 200% of Spanish minimum wage (approximately €2,850-€3,024 per month for 2026), plus proof that your employer is based outside Spain and that you've worked remotely for at least 12 months prior to application.

Other pathways include the Family Reunification Visa for spouses and children of Spanish residents (no specific financial requirement, but the sponsoring resident must prove adequate housing and income), and entrepreneur visas for those Starting business in Spain (requires detailed business plan and typically €50,000+ in startup capital). For comprehensive analysis of all options, see our complete guide to Spanish visas.

How long can I live in Spain without becoming a tax resident?

Spanish tax residency is determined by the 183-day rule—you become a Spanish tax resident if you spend more than 183 days in Spain during a calendar year, or if Spain is your "center of economic interests" (meaning your primary income sources or business activities are based in Spain). Tax residency triggers the obligation to declare and pay Spanish taxes on your worldwide income, not just Spanish-source income.

For non-residents who want to maximize time in Spain without triggering tax residency, the safest approach is to stay clearly under 183 days in any calendar year and to avoid shifting your main economic or professional activities to Spain. You should also keep detailed records of travel dates and consult a cross‑border tax advisor if you are close to the 183‑day threshold or have significant Spanish‑source income.